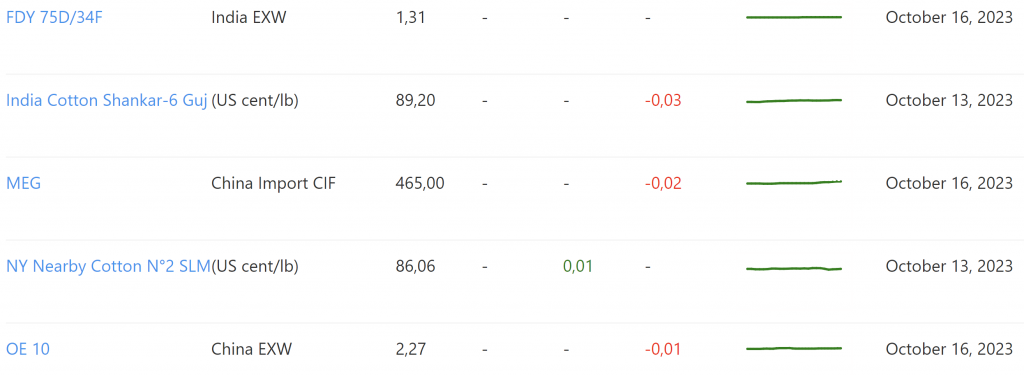

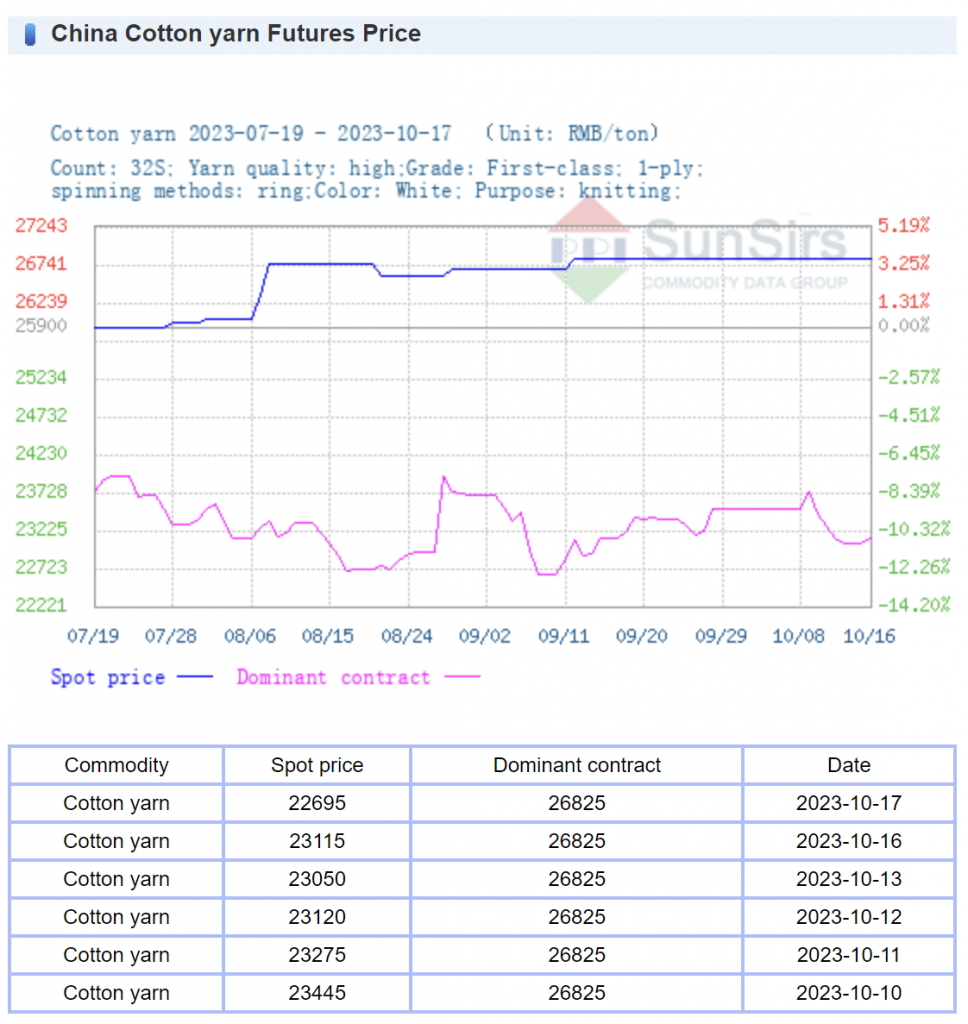

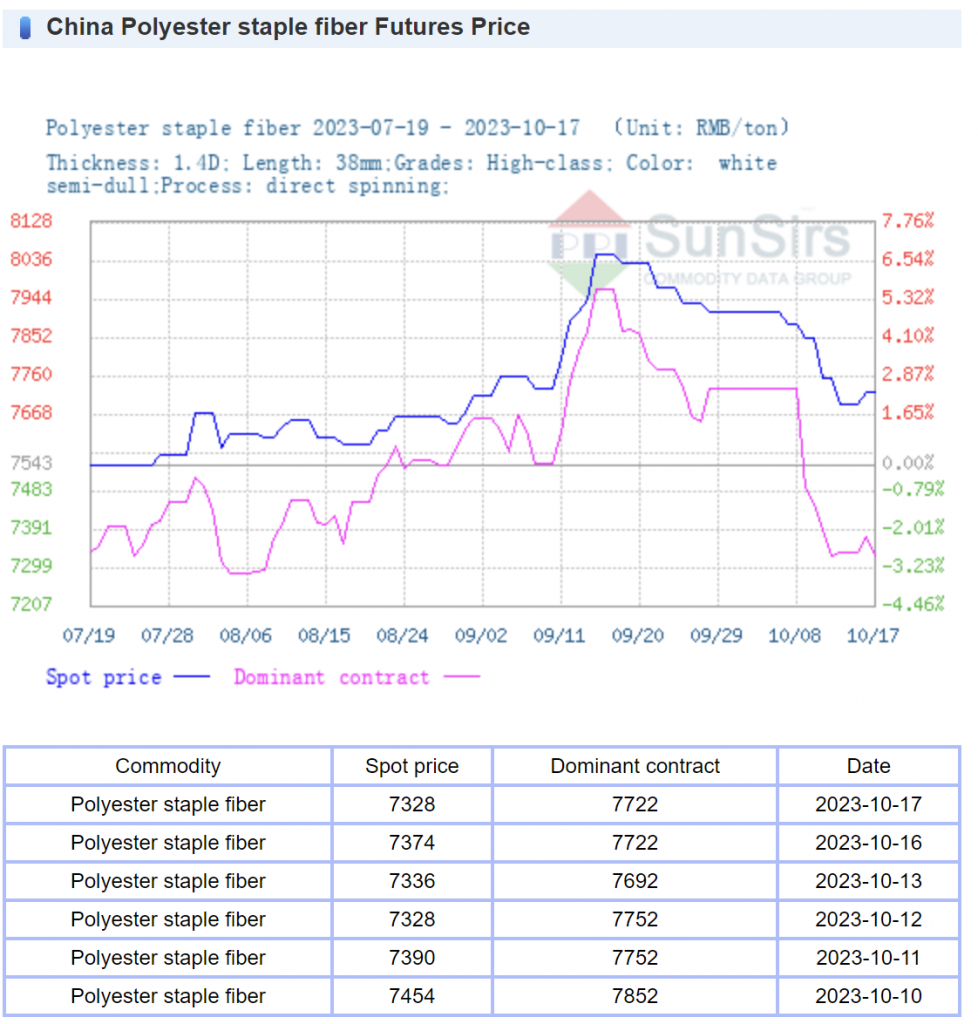

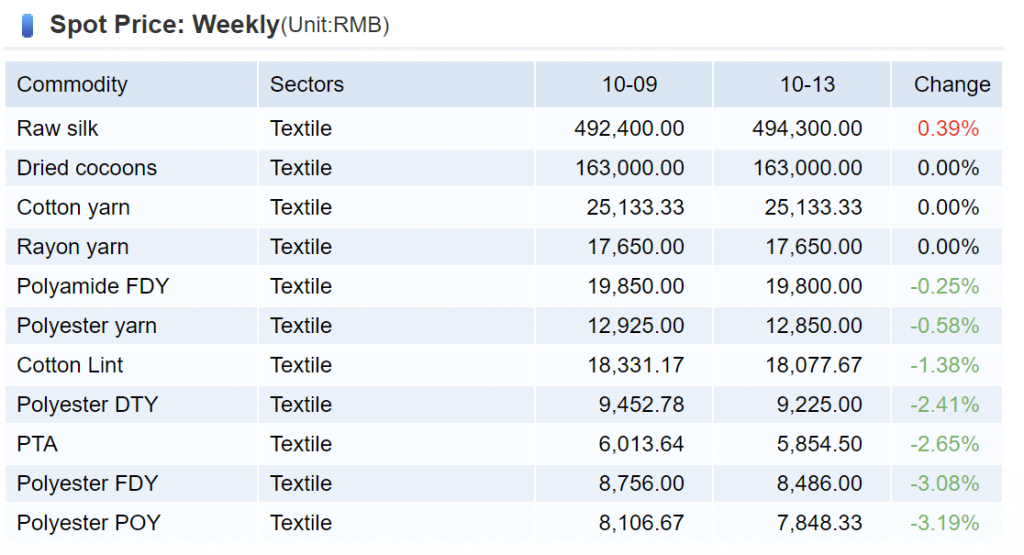

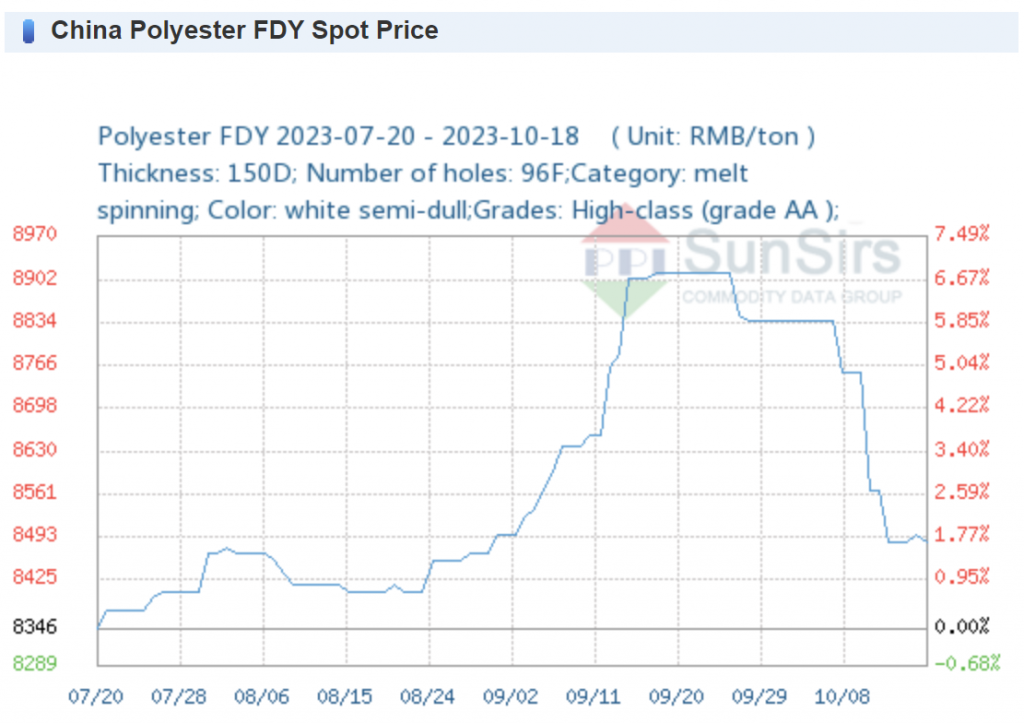

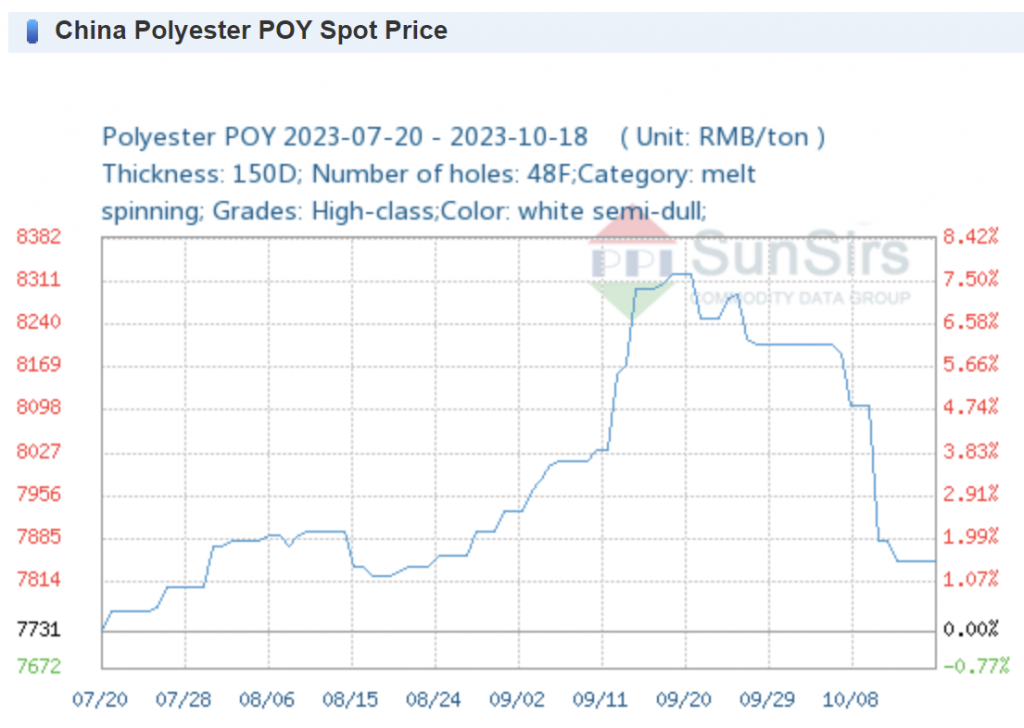

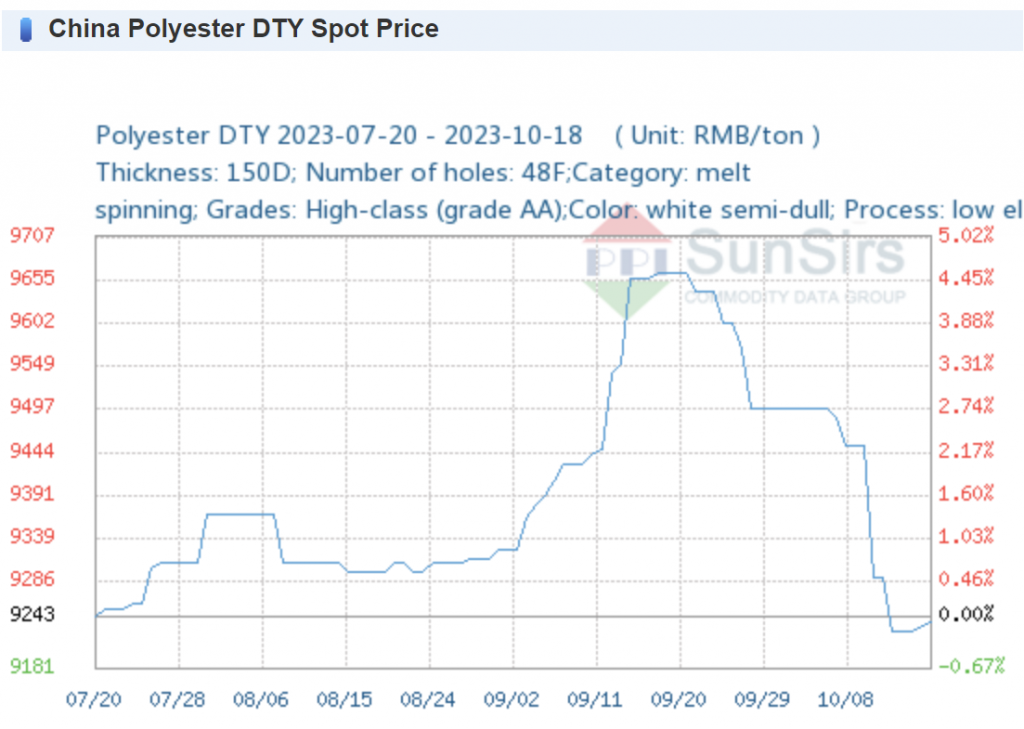

1. GIÁ CẢ THỊ TRƯỜNG

2. BIẾN ĐỘNG GIÁ

3. TIN THỊ TRƯỜNG

Triển vọng bông 2023/24: Việc cắt giảm sản lượng tại Mỹ, những thay đổi toàn cầu và ổn định giá cả

Triển vọng bông Mỹ (2023/24)

- Giảm sản lượng: Sản lượng bông của Mỹ niên vụ 2023/24 thấp hơn 315.000 kiện so với ước tính tháng trước, đạt tổng cộng 12,8 triệu kiện. Mức giảm này là do sản lượng thấp hơn ở Texas, bù đắp cho sự gia tăng ở những nơi khác.

- Giảm xuất khẩu: Xuất khẩu bông niên vụ 2023/24 dự kiến sẽ giảm 100.000 kiện xuống còn 12,2 triệu kiện.

- Tồn cuối kỳ giảm: Do sản lượng giảm và xuất khẩu giảm, tồn cuối kỳ giảm 200.000 kiện.

- Dự báo giá ổn định: Giá trung bình bông upland mùa 2023/24 dự kiến sẽ không thay đổi so với tháng trước ở mức 80 cent mỗi pound. Mức giá này thấp hơn gần 5 cent so với giá cuối cùng của mùa 2022/23 (84,8 cent mỗi pound).

Triển vọng bông toàn cầu (2023/24)

- Tồn đầu kỳ giảm: Tồn kho bông toàn cầu đầu kỳ niên vụ 2023/24 thấp hơn 10,3 triệu kiện so với ước tính tháng 9, đạt tổng cộng 82,8 triệu kiện. Việc giảm lượng tồn kho lớn là do những thay đổi liên quan đến Brazil, bắt đầu từ vụ 2000/2001.

- Tồn cuối kỳ thấp hơn: Bảng cân đối toàn cầu niên vụ 2023/24 cho thấy tồn kho cuối kỳ giảm 10 triệu kiện, cũng do thay đổi liên quan đến Brazil. Sự thay đổi này phản ánh thời điểm thu hoạch của Brazil và dẫn đến việc điều chỉnh bảng cân đối.

- Sản lượng bông của Brazil tăng: Ước tính vụ mùa bông Brazil 2023/24 của USDA đã tăng thêm 160.000 kiện, lên tổng số 14,56 triệu kiện. Việc điều chỉnh này dựa trên kết quả đánh giá do Companhia Nacional de Supply (CONAB) của Brazil thực hiện vào ngày 10 tháng 10.

- Những thay đổi nhỏ trên toàn cầu: Có những thay đổi nhỏ trong bảng cân đối bông toàn cầu 2023/24. Sản lượng toàn cầu đã tăng 210.000 kiện kể từ tháng 9, chủ yếu do vụ thu hoạch lớn hơn ở Brazil, Argentina và Tanzania, bù đắp cho mức giảm ở Mỹ, Australia và Hy Lạp. Tiêu thụ và thương mại toàn cầu giảm nhẹ lần lượt là 89.000 và 35.000 kiện.

Ngọc Trâm (theo Investing)

*************

Cotton’s 2023/24 Outlook: Reduced U.S. Production, Global Changes, and Price Stability

U.S. Cotton Outlook (2023/24)

- Lower Production: The 2023/24 U.S. cotton production is 315,000 bales lower than the previous month’s estimate, totaling 12.8 million bales. This decrease is attributed to lower yields in Texas, which offset gains in other regions.

- Reduced Exports: Cotton exports for the 2023/24 season are projected to be 100,000 bales lower, down to 12.2 million bales.

- Lower Ending Stocks: Due to the lower production and reduced exports, ending stocks are reduced by 200,000 bales.

- Stable Price Forecast: The season-average price for upland cotton in 2023/24 is forecast to remain unchanged from the previous month at 80.0 cents per pound. This price is nearly 5 cents below the final price for the 2022/23 season, which was 84.8 cents per pound.

Global Cotton Outlook (2023/24)

- Reduced Beginning Stocks: World beginning stocks of cotton for the 2023/24 season are 10.3 million bales lower than the September estimate, totaling 82.8 million bales. This significant reduction is primarily due to an accounting change related to Brazil, dating back to the 2000/01 season.

- Lower Ending Stocks: The world balance sheet for 2023/24 shows a reduction of 10.0 million bales in ending stocks, also because of the accounting change related to Brazil. This change reflects the timing of Brazil’s harvest and has led to adjustments in the balance sheet.

- Brazil Crop Increase: The estimate for USDA’s 2023/24 Brazil cotton crop has been increased by 160,000 bales, totaling 14.56 million bales. This adjustment is based on a revision made by Brazil’s Companhia Nacional de Abastecimento (CONAB) on October 10.

- Minor Global Changes: There are small changes in the world 2023/24 cotton balance sheet. Global production has increased by 210,000 bales since September, primarily due to larger crops in Brazil, Argentina, and Tanzania, which offset reductions in the United States, Australia, and Greece. World consumption and trade have seen minor reductions of 89,000 bales and 35,000 bales, respectively.

Source: Investing

==============

- Price database is referenced from domestic market of China, India, Pakistan, Bangladesh .

- The unit price of yarn referred from Chinese market and other countries which is different from the unit price of yarn produced in Vietnam, so please refer to the weekly price data and historical price fluctuations for the range of market price fluctuations per period.

- The article analyzes, comments and evaluates the market price referenced from many sources. Translated and edited by VCOSA in Vietnamese. There is always an original to compare just below each news.

- Some yarn price information is hidden for privacy (VCOSA members only), for more information, please call our hotline at + 84-902379490.

- Website www.vietnamyarnprice.com has officially launched. Portal to look up and share prices of the yarn industry in Vietnam and other countries.