Polyester filament prices have heavily fallen in the past seven days in China, reflecting a weaker seasonal demand than usual from filament fabric producers. PSF prices have more resisted however, also confronted with a poor demand level from spinners.

Polyester filament prices have significantly dropped in the last seven days in China whereas staple fiber prices have continued slightly declining.

Benchmark 1.4D PSF has lost 110 yuan per metric ton or 1.2%. This is still a relatively negligible decline, however indicating the weakness of downward textile production.

The seasonal peak of March-April has been lower than in past years, leaving spinners with large inventories.

The filament weaving activity has even more suffered, and prices of filament yarns have therefore plunged over a fall in sales.

The POY benchmark indicator has declined 420 yuan per MT or 4.5% in a single week, whereas FDY was losing 320 yuan or 3% and DTY 350 yuan or 3.4%.

Filament prices could further decline in the coming period, as operating rates have not yet been lowered at polyester fiber plants.

Enjoying ample margins, fiber producers may accept reducing their prices rather than cutting their operating rates.

PTA prices have not risen in the past two weeks in addition, and the fall of margins remains relatively limited at PSF plants, although more significant at filament plants.

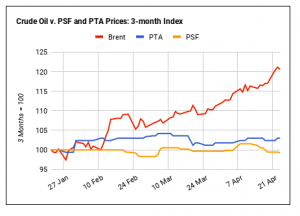

The current rebound of crude oil prices is fully absorbed by paraxylene producers, who currently are the weakest link of the polyester chain.

PTA producers could be forced to cut their operating rates in the coming weeks however, if PX prices would stop falling over a drop of paraxylene production.

In the meantime, demand for polyester will not rebound, meaning that prices could further fall.

Source: Emergingtextiles