Polyester intermediate prices have stayed relatively firm in the past week, whatever the fall of paraxylene prices over the addition of new production capacities in China. Operating rates are reaching record levels at polyester plants where profit margins are also further rising.

Polyester chain prices are currently supported by a strong seasonal demand from downward processors in the textile industry whereas crude oil prices are staying very firm at their higher levels.

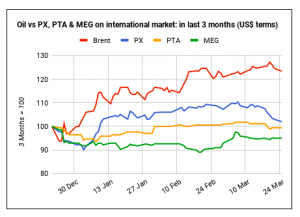

PTA and MEG prices have remained relatively unchanged on spot markets in the past week, although paraxylene prices have further declined.

Spot PX prices have fallen to 1,028$ per metric ton FOB Korea (1,048$ CFR Taiwan), a weekly decline of 5.2%.

Paraxylene is back to a level not seen since January 10th when FOB Korea had eventually climbed above 1,000$, over a rebound of crude oil prices.

The oil market remains currently supported by production cuts in Saudi Arabia, but prices could eventually fall in the coming months, as production is rising elsewhere.

Lower profits at PX plants

Whatever the strength of crude oil prices, paraxylene prices are however falling in line with the commissioning of new capacities in China.

Hengli just announced the successfull start of production at its giant petrochemical complex in Dalian, including 2.2 million tons of PX capacities per year.

With prices falling and material costs rising, profits have further declined at PX plants with PX/Naphtha spread losing 16.6% in four weeks.

Demand remains however strong from PTA plants where operating rates have stayed at a high level, thanks to the fall of paraxylene prices.

Margins of PTA producers are rising with PX/PTA spread down 25% in four weeks.

MEG remains firm, but could drop

MEG prices are currently very firm after showing signs of a long-term decline which could however resume in the coming weeks.

Seasonal demand is low after the end of the winter, depressing sales of antifreeze, and ahead of the summer with demand for PET bottle packaging not yet rebounding.

Demand from polyester plants is however very strong, after their operating rates have further risen to 89% at the end of last week, an extremely high level by historical standards.

Margins of polyester producers have further improved as PTA prices have not increased and staple fiber and filament yarns have slightly climbed.

Source: Emergingtextiles