Polyester chain prices have fallen across the board over the weekend with most petrochemical products eventually declining 15-20% in two weeks. PTA prices have heavily dropped, leaving room for further lowering polyester prices in the coming period.

Polyester chain prices have heavily fallen in the last two days, in line with a looming geopolitical crisis between the United States and China.

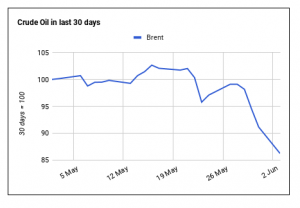

As a clear sign that pessimism prevails, crude oil prices have tumbled in the last two weeks, with New York’s WTI plunging by 16%.

Other petrochemical products in the polyester chain have followed the same downward way.

Naphtha CFR Japan has even declined below 500$ per metric ton this Monday, therefore losing 19.5% in two weeks.

MX and PX prices have respectively dropped by 5% and 2.8% in the last seven days.

At the same time, PTA prices have sharply fallen, being down 2.5% over the weekend on the international market and losing 2.8% on the domestic market in China.

In two weeks, PTA prices have declined 6.1% on the international market and even 9.7% in China.

Polyester staple fiber prices have also heavily decreased in the past two weeks, but polyester filament prices have been supported by anticipations of a possible rebound in prices which has not occurred.

PSF prices have lost nearly 10% in two weeks, but the decline of filament prices has only reached 4.5%.

The fall of material costs at polyester plants should trigger a new decline of fiber prices, as demand will not immediately rebound, being depressed by seasonal trends and widespread pessimism in the textile and apparel industries in China.

The deterioration of US-China relations could now really affect the textile and apparel trade on the global market, if the Trump administration eventually decides to raise by 25% US import tariffs on Chinese apparel.

A global economic slowdown would also depress petrochemical prices over the coming period with polyester prices therefore falling to historically low levels.

Source: Emergingtextiles