Raw material costs of polyester fiber producers are weakening in the current period whatever the rebound of crude oil, naphtha, mixed xylene and paraxylene prices in the past two weeks. Downward textile producers are far from enthusiastic, in addition, although optimism is back in China’s economy.

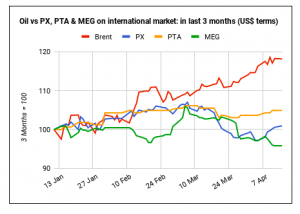

Paraxylene prices have clearly risen in the past weeks in the Far East.

From a low at $1,017 per metric ton on March 28th, the FOB Korea price has climbed to 1,049$ or 3.15% in slightly more than two weeks.

This is not a sharp increase, but far from the decline which had been previously observed for weeks.

Crude oil prices have rebounded in the last weeks, over new production cuts planned by producers and lower inventory levels.

The rebound of oil prices is however not the main factor behind the rise of paraxylene which is mostly driven by tighter supply in Asia.

Operating rates are expected dropping in China over a series of overhauls planned for the second part of April.

PX sales could however be weaker to PTA producers who are also expected triggering a series of maintenance operations resulting in lower demand for raw materials.

More importantly, sales of polyester fibers have reportedly weakened in the last week in China.

PTA prices have gained 5$ CIF China in the last seven days, however losing 70 yuan on the domestic market.

Downward textile producers are not enthusiastic whatever the return to optimism in the country.

The MEG market has remained heavily depressed in addition, with prices losing 15$ in a single week or 2.45%.

Polyester fiber prices could weaken in the coming period, in line with a very high level of operating rates currently above 90% in China.

Source: Emergingtextiles